IGNOU BCOC-136- Solved Assignment

Are you looking to download a PDF soft copy of the Solved Assignment BCOC 136 Income Tax Law and Practice is the right place for you. This particular Assignment references the syllabus chosen for the subject of Hindi, English, for the Jul 25 – Jan 26, Jul 24 – Jan 25 session. The code for the assignment is BCOC-136 and it is often used by students who are enrolled in the BSC (Honours), IGNOU CBCS Solved Assignments Degree. Once students have paid for the Assignment, they can Instantly Download to their PC, Laptop or Mobile Devices in soft copy as a PDF format. After studying the contents of this Assignment, students will have a better grasp of the subject and will be able to prepare for their upcoming tests.

PLEASE MATCH YOUR ASSIGNMENT QUESTIONS ACCORDING TO YOUR SESSION

IGNOU BCOC-136 (July 2025 – June 2026) Assignment Questions

1. a) “The income of the previous year is taxed in the current year”. Explain.

b) Explain the provisions of Income Tax Act for an individual, if he is a a) Resident b) Not Ordinarily Resident c) Non-Resident.

2. a) Define annual value and state the deductions that are allowed from the annual value in computing the income from house property.

b) Explain the procedure for E-filing of ITR in India?

3. Write short note on following:

a) Partial Integration of Agricultural and Non-Agricultural Income.

b) Deduction u/s 80G.

c) Provisions for calculating House rent allowance

d) Encashment of Earned Leave on Retirement

4. Mr. Nagraj, who is not covered under Payment of Gratuity Act, retires on 25 December, 2023 from ABC Ltd. After the service of 36 years 9 months. He received gratuity amount of Rs 5,00,000. His salary is Rs. 6,000 per month up to June 30, 2023 and 7,000 per month from July 2023. He also gets D.A. of Rs. 1,000 per month (70% of which is considered for service benefit). Find the taxable amount of Gratuity for the A.Y. 2024-25.

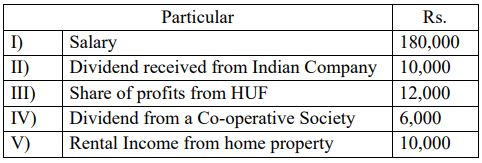

5. Compute the total income and tax liability of Mr. X aged 60 years, a professor at a college affiliated to Delhi University, for the assessment year 2024-25 on the basis of the following particulars (calculate as per old tax regime):

6. Explain the following:

a) Bond washing Transaction

b) ITR-1 (SAHAJ)

c) Provisions of the Income Tax Act regarding exemption of capital gains u/s54F

d) Rent Free Accommodation

IGNOU BCOC-136 (July 2024 – June 2025) Assignment Questions

Section-A

(Attempt all the questions. Each question carries 10 marks.)

1. Explain the procedure for E-Filing of Return.

2. Explain the provisions relating to House Rent Allowance u/s 10 (13A)

3. Explain the certain incomes for which the tax is paid in the same year

4. Explain the provisions relating to exemption of incomes of Charitable and Religious Trust and a Political Party

5. Compute the total Income of Mr. Manas from the following particulars of his income for A.Y. 2023-24.

Section-B

(Attempt all the questions. Each question carries 6 marks.)

6. Explain the Provisions of commutation of Pension u/s 10 (10A)

7. What is ITR-1 (SAHAJ)?

8. Write the Provisions relating to Clubbing of minor’s income

9. Explain the Provisions relating to Gratuity u/s 10(10) in case of employees is covered by Payment of Gratuity Act, 1972.

10. After 25 years stay in India, Mr. Ram went to U.S.A. on April 15, 2012 and came back to India on March 12, 2023. Determine his residential status for the assessment year 2023-24.

Section-C

(Attempt all the questions. Each question carries 5 marks.)

11. Write short note on following:

a) Partial Integration of Agricultural and Non-Agricultural Income.

b) Deduction u/s 80D.

c) “Defective return is no return”

d) Standard Deduction u/s 16(i)

IGNOU BCOC-136 (July 2025 – June 2026) Assignment Questions

1. क) ‘गत वर्ष की आय पर कर निर्धारण वर्ष में कर लगाया जाता है व्याख्या कीजिए।

ख) व्यष्टि (individuals) के सम्बन्ध में निम्नलिखित का स्पष्टीकरण कीजिए : i) निवासी ii) मामूली तौर पर निवासी नहीं iii) अनिवासी

2. क) वार्षिक मूल्य को परिभाषित कीजिये तथा मकान सम्पत्ति से आय निर्धारित करने के लिये वार्षिक मूल्य से दी जाने वाली कटौतियों का वर्णन कीजिये।

ख) भारत में आईटीआर की ई-फाइलिंग की प्रक्रिया की व्याख्या करें?

3. निम्नलिखित पर संक्षिप्त टिप्पणी लिखेंः

क) कृषि आय और अंशतः कृषि आय

ख) धारा 80जी के तहत कटौती।

ग) मकान किराए भत्ते से संबंधित आयकर के प्रावधान

घ) सेवानिवृति पर अर्जित अवकाश का नकदीकरण

4. श्री नागराज जो ग्रेच्युटी भुगतान के अंतर्गत नहीं आते हैं। 25 दिसंबर 2023 को ABC लिमिटेड से 36 वर्ष 9 माह सेवा करने के बाद रिटायर हुए और ग्रेच्युटी का रु 5,00,000 प्राप्त किया उनका वेतन 30 जून 2023 तक रु. 6,000 प्रति माह तथा उसके बाद जुलाई 2023 से रु. 7,000 प्रति माह हो गया उन्हें महंगाई भत्ता भी रु. 1,000 प्रति माह की दर से मिलता था जिसका 70% सेवा की शर्तों के अधीन था कर निर्धारण वर्ष 2024-25 ग्रेच्युटी की कर योग्य राशि की गणना कीजिए।

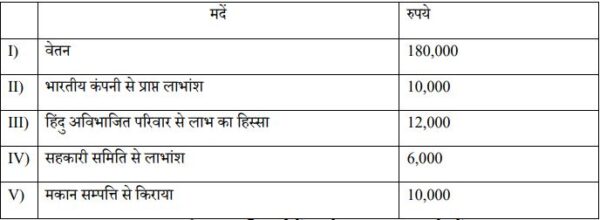

5. निम्न सूचना के आधार पर दिल्ली विश्वविद्यालय के 60 वर्षीय प्रोफेसर श्री x की कर निर्धारण वर्ष 2024-25 के लिये कुल आय तथा देय कर की गणना कीजिये। (पुरानी कर व्यवस्था के अनुसार गणना करें):

6. निम्नलिखित को स्पष्ट करे:

क) दिखावटी लेन देन (Bond Washing Transaction)

ख) आईटीआर-1

ग) आयकर अधिनियम की धारा 54 F के अन्तर्गत वर्णित करमुक्त पूँजी लाभ से सम्बन्धित प्रावधान

घ) किराया मुक्त आवास

IGNOU BCOC-136 (July 2024 – June 2025) Assignment Questions

खण्ड – क ( सभी प्रश्न अनिवार्य हैं। प्रत्येक प्रश्न 10 अंक के हैं)

1. रिटर्न दाखिले की ई फाईलिंग के प्रावधानों की चर्चा कीजिए।

2. मकान किराया भत्ता संबंधित प्रावधानों को समझाइए ।

3. ऐसे कुछ आयों को समझायें जिसका कर उसी वर्ष चुकाया जाए जिस वर्ष अर्जित किया है।

4. पुण्यार्थ तथा धार्मिक न्यास और राजनीतिक दलों को करमुक्त आय के प्रावधानों को समझाये।

5. निम्नलिखित विवरणों से कर निर्धारण वर्ष 2023-24 के लिए श्री मानस की कुल आय की गणना कीजिए ।

खण्ड ख (सभी प्रश्न अनिवार्य हैं। प्रत्येक प्रश्न 6 अंक के हैं)

6. धारा 10 (10 A) के अंतर्गत पेंशन के प्रावधान को समझाये ।

7. ITR – I सहज (SAHAJ) फॉर्म क्या है ?

8. अवयस्क की आय के मिलान संबंधी प्रावधान क्या है ?

9. यदि कर्मचारी ग्रेच्युटी अधिनियम 1972 के अंतर्गत आते हैं तो धारा 10 (10) के अंतर्गत ग्रेच्युटी के प्रावधान की व्याख्या करें।

10. श्री राम भारत में 25 वर्ष रहने के उपरांत 15, अप्रैल 2012 के यू. एस. ए. चले गए और भारत वापस मार्च 12, 2023 में आये । करनिर्धारण वर्ष 2023-24 के लिए उनकी निवासीय स्थिति ज्ञात करें।

खण्ड – ग (सभी प्रश्न अनिवार्य हैं। प्रत्येक प्रश्न 5 अंक के हैं)

11. निम्नलिखित के संक्षिप्त उत्तर लिखिये :

(क) अंशत: सम्मिलित कृषि एवं गैर कृषि आयों के प्रावधान बताये ।

(ख) धारा 80 D के अंतर्गत कटौती को समझाये।

(ग) दोषपूर्ण रिटर्न को रिटर्न नहीं माना जाता है, समझाये ।

(घ) धारा 16 (1) के अंतर्गत प्रमाणिक कटौती के प्रावधानों को बताये।

IGNOU BCOC-136 ASSIGNMENTS DETAILS

| University | : | IGNOU (Indira Gandhi National Open University) | |

| Title | : | Income Tax Law and Practice | |

| Language(s) | : | English, Hindi | |

| Code | : | BCOC-136 | |

| Degree | : | BCOMF, BCOMG | |

| Subject | : | Business and Law | |

| Course | : | Core Courses (CC) | |

| Author | : | ignouedumart.com Panel | |

| Publisher | : | Distance Gyan Publishing House Pvt. Ltd. |

Call us: +91 9466323363

Reviews

There are no reviews yet.